Reimbursement and the Revenue Cycle

Reimbursement

Reimbursement is a payer system to pay for services provided within a provider organization. Reimbursement tools and systems aim to establish the final cost and implement payment. On the provider side, attention must be paid to how the service is provided and how it reflects the actual need for the service (Freidson, 2017). Payments must be made on time, so the provider organization receives funds to process new patient requests. Third parties can verify that payments are correct and evaluate the quality of services to the cost. Any changes in the reimbursement process can cause delays and change the speed and timing of payment transfers to the organization.

The reimbursement fee is a relatively large amount of money that the provider organization uses for several purposes. First, it is budgeting for resources: equipment, instruments, disposable hygiene items, medications, hospital beds, and all the supplies needed to run the hospital. Second, there are employee benefits: the staff is large enough that hospitals must pay a decent wage for their work. Third, government fees and taxes allow providers to receive grants, additional funding, and participation in national systems. If an organization does not receive compensation payments, it loses a significant source of income. The resources to provide services will be reduced: the organization will not be able to purchase equipment, equip hospital beds, or purchase medications or dressings. As a result, the hospital’s capacity will be reduced, resulting in financial hardship.

The Revenue Cycle

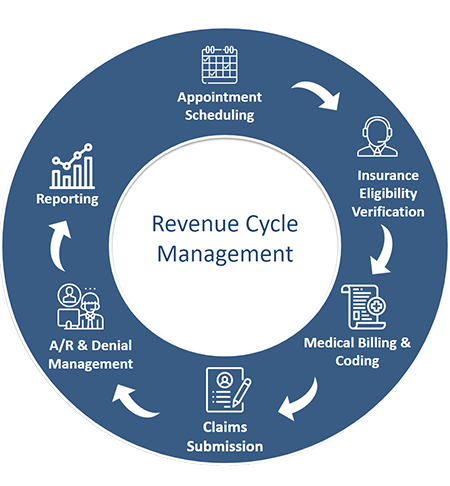

Revenue Cycle Management (RCM) is a dynamic process that healthcare facilities use to track patient revenue. RCM combines all of the administrative procedures (enrollment, processing, filling out forms) and the clinical services provided to the patient (Derricks, 2021). The cycle begins in pre-authorization, where patient information is collected, and initial paperwork is completed; the end is in reporting, where the totals of all RCM steps are collected. Image 1 shows the RCM with the steps the patient moves through.

The process can be divided into four periods: registration, service performance, coding, and billing. The registration phase collects patient data, which is necessary to refer the patient according to patient capacity (Freidson, 2017). The stage is necessary to evaluate certifications and providers and establish pricing policies. The billing stage is where care is directly performed, after which the coding stage begins, where all procedures are translated into a set of numbers and letters. This data reflects the coding and billing process, so one must pay the most attention to it. Finally, the provider bills the patient or their payer, who must make payment according to the code (Freidson, 2017). A final step can be highlighted, where the payment status is assessed and confirmation that the patient has received their services.

All departments are included in RCM, but they play different roles in the final billing. First and foremost, registration must be given attention for proper billing (Derricks, 2021). The staff must collect the information and fill it out. Second, the coding and billing department handles the reconciliation of the service and estimated cost. It is an important step in verifying the payment data given to the payer. Finally, the order processing and auditing department establish that the payment has been completed and verified (Melling, 2017). The department must do a final verification of service and payment compliance and to report on the services performed.

Departmental Impact on Reimbursement

Reimbursement Data

Reimbursement data is all the data that comes into the medical organization, thus forming the basis for determining the potential budget of the provider in the following year. It is monitored internally and by third parties who match the services performed to the payment received (Melling, 2017). Third-party and recovery audit contractors (RACs) perform payment verification to avoid fraud, abuse, and patient or payer violations (Recovery Auditors / RACs, n.d.). Collecting reimbursement data is a safety net for all parties and a picture of the actual situation regarding costs.

If providers fail to collect reimbursement data, they may face low revenues. Sometimes the payer sends back payment forms, and some invoices may not be held – without collecting the information, the vendor will not know (Burks et al., 2022). The lack of data can lead to additional costs in resolving claims from the payer who disagrees with the organization’s reported rates. Currently, programs such as pay-for-performance will improve organizations’ performance (Catalano, 2009). The visibility will determine if the services are valuable in care and future collaboration with patients or payers.

Department Tasks

The Registrar’s Office collects objective data about the patient: medical registrars must collect information to bill the patient based on insurance correctly. If the forms are filled out incorrectly, the organization risks being fined and suspended from insurance payers for unintentional fraud (Faux et al., 2021). The registrars take on the responsibility of transmitting data to all the following departments: they contract and schedule patients based on the value of services.

The coding and billing department is responsible for coding information from clinical language to financial language. It is a secondary control for the data transmitted to insurance companies (Burks et al., 2022). Specialists must reconcile the code and service cost and ensures that all services have been performed correctly. This department determines what information the insurance company receives and whether it is complete and correct.

The medical personnel who provide the services ensure that they are performed entirely. On the part of the clinical units, it is necessary to determine the actual need for the service. They obtain informed consent from patients that they understand the need to pay for services (Esposito et al., 2020). It avoids miscommunication and builds a good attitude toward the billing process. All departments are linked together by the administration, who direct and organize communication processes within the hospital.

Ensuring Compliance with Billing and Coding Policies

Billing and coding policy compliance is verified by the appropriate department that implements these procedures. They reconcile current legislation regarding coding policies and relay this information to co-located individuals (Harrington, 2019a). The staff conducts internal and general audits to determine staff actions for compliance with the organization’s regulatory standards. The billing and coding department provides the organization with national health care regulations and standards and works with the administration to negotiate with payers to establish pricing policies.

If the department fails to fulfill its responsibilities, the organization runs the increased risk of being fined or suspended from its operations. A provider may lose its place in the service market because payers will not want to pay for services that are not performed to standards. The lack of compliance with policy and actual service delivery will lead to liability and a lack of budget for the current and next year (“Systems of care compliance program,” 2021). The department impacts the organization by generating reportable plans and providing staff with timely policy summaries. In addition, the department influences the overall status of the provider, based on which other payers want to enter into new contracts.

Billing and Reimbursement

Third-Party Policy

Patient financial services (PFS) is a patient support service that allows patients to get up-to-date information on the cost of services, adjust the assignment of payments to their insurance companies, and find out the status of payments. Third-party payers are brought in to work with PFS to set up communication channels with the provider for patients (Harrington, 2019c). The policies they create shape when payments are received, how long they take to process, how claims are negotiated, and how penalties are reimbursed. Contracts with third-party payers highlight categories of payments that contain errors or are clean and subject to normal transaction pathways.

In cooperation with third-party payers, PFS establishes the rules for signing contracts and the terms and conditions for its performance and termination. Based on contracts and the Affordable Care Act, patients can choose their providers, so it is in the organization’s best interest to seek out payers with transparent policies and financial accountability (Harrington, 2019a). To avoid additional costs and penalties, providers should evaluate third-party payer policies and be cautious of their questionable offerings.

Areas of Analysis for Maximization and Timeliness of Reimbursement

- Creating an accurate and reliable source of information ensures complete consistency between the data being transmitted and received.

- Evaluating compliance based on a coding system for reporting and verifying information (Harrington, 2019b).

- Conducting logistical transactions through PFS to ensure patients and payers have all information according to their financial capacity.

- Analyzing checks and payments to generate reports on the number of correctly made, rejected, and erroneous payments.

- Evaluating rejected and ignored claims to determine reasons for ignoring and getting the total amount.

The Way of Structuring Personnel

For reimbursement processes to work effectively there is a process structure that considers each step in RCM. A process structure emphasizes process and establishes strict hierarchical principles that maximize efficiency (Lawrence et al., 2019). With the help of benchmarks and indicators, general managers monitor ongoing work and direct personnel to the sagging elements of the process. This structure requires managers to analyze a lot of data, which is not always possible in a one-person operation. Specialized software and computational intelligence tools are recommended to overcome this obstacle. In addition, exceptional managers can be assigned to monitor process performance (Lawrence et al., 2019). The use of checkpoints and input-output tracking will help to validate the effectiveness of the process structure.

Periodic Procedure Revision Plan

A periodic procedure revision plan is necessary to track compliance with internal billing and reimbursement policies. First, attention must be paid to internal auditing and monitoring to ensure that the organization is legally and ethically informed about regulatory quality standards for services and procedures (Herzig & Walsh, 2020). Second, one should turn to modern compliance monitoring tools, including various IT products that allow for quick dissemination of information within the department and monitoring performance (e.g., through checklists). Third, the organization can use training and educational events with invited employees and contractors who will track and verify performance (Faux et al., 2021). Finally, an audit based on current law with outside observers.

Such a plan will build a picture of why procedures must be followed according to the organization’s policies in the first place. It will shift the focus from simple payments to an analytical view of reimbursement and shape the organization’s business environment (Herzig & Walsh, 2020). Internal assessment tools are likely helpful, but attention is needed to monitor these checks and ensure they are accurate.

Marketing and Reimbursement

Managed Care Contracts

Managed care is a new approach to providing services designed to control cost growth. There are four managed care packages, differing in when, when, and for what reasons payment is made. The new contracts directly affect how the provider organization will be reimbursed and how costs will be calculated: before the service is provided or after (Harrington, 2019c). The new contracts form a unique approach based on the service’s value rather than the usual provision. These contracts greatly simplify procurement processes and control the flow of resources and service costs. It has been noted that it reduces the re-hospitalization rate and shortens the time it takes to receive care (Dugan, 2020). Finally, the new contracts increase provider referrals and create transparent policies for both parties.

Resources to Ensure Billing and Coding Compliance

First, the provider organization must look at the human resources – the staff – that are the primary source of both positive and negative outcomes. The organization must ensure that staff understands their responsibilities and, if possible, conduct additional training courses to increase the awareness of coding professionals (“Systems of care compliance program,” 2021). In addition, providers should engage the finance department to direct the budget to create communication with payers and patients. Monetary motivation should not be neglected; often a companion to well-organized work. Once a quarter, there should be an evaluation of how employees use the resources allocated to communication development.

Suppliers need to pay attention to how billing and coding policies are written. It should be developed by legislation that describes the standards for service delivery and coding (Harrington, 2019a). Providers risk being fined or dropped from a particular insurance program if these requirements are unmet. Sometimes providers outsource as support, but it is essential to ensure that the organization has the financial and administrative capacity to support third-party contractors.

Organizations must employ control tools to assess compliance. These include fraud and abuse prevention (quality control department), input and output analysis (error control), and an internal business structure evaluation team. While the first two elements are apparent, the professional (including ethical) assessment of personnel actions is far from always successful for suppliers (Shapiro et al., 2018). It is essential to regularly assess the internal culture and conditions that contribute to policy compliance: company openness, communication and feedback, and corporate virtues. These elements will help orient employees to a responsible and welcoming approach to work.

Strategies for Complying with Ethical Standards

Ethical standards in reimbursement are as crucial as analytical financial tools. They ensure that generally accepted standards in communication and trust building are followed. These standards are especially needed when negotiating and dealing with stakeholders (“Systems of care compliance program,” 2021). Suppliers must be assured that outside observers will not be disruptive or disruptive to the organization. Stakeholders in reimbursing services are providers, patients, and payers themselves.

In order to meet ethical standards within the organization, it is necessary to focus on a strategy that implies the development of business culture. High ethical standards will be achieved when the staff understands their necessity (Harrington, 2019b). In particular, this can be done through business counseling and staff unification. In addition, training is needed to ensure that staff communicates and records information without outside intent.

For patients, the reimbursement process is usually through the payer, but they must meet ethical standards by providing all information. Patients need to be legally supported to avoid inadvertent malpractice that would lead to financial loss. This strategy is consistent with a social benefit strategy for payers: Providers must create the conditions for insurance companies to be predisposed to pay (Shapiro et al., 2018). It is achieved through transparent organizational policies that ensure that all services are reasonable and that staff does not exceed their authority.

References

Burks, K., Shields, J., Evans, J., Plumley, J., Gerlach, J., & Flesher, S. (2022). A systematic review of outpatient billing practices. SAGE open medicine, 10.

Catalano, K. (2009). Pay-for-performance and recovery audit contractors: The whys and wherefores of these programs. Plastic Surgical Nursing: Official Journal Of The American Society Of Plastic And Reconstructive Surgical Nurses, 29(3), 179–182.

Derricks, J. (2021). Overview of the claims submission, medical billing, and revenue cycle management processes. In: Szalados, J.E. (eds), The medical-legal aspects of acute care medicine. Springer, Cham.

Dugan J. A. (2020). Fixed effects analysis of the incidence of cardiovascular outcomes under managed care following the managed care backlash. Medicine, 99(23), e20636.

Esposito, T., Reed, R., Adams, R. C., Fakhry, S., Carey, D., & Crandall, M. L. (2020). Acute care surgery billing, coding and documentation series part 2: Postoperative documentation and coding; documentation and coding in conjunction with trainees and advanced practitioners; coding select procedures. Trauma surgery & acute care open, 5(1), e000586.

Faux, M., Adams, J., & Wardle, J. (2021). Educational needs of medical practitioners about medical billing: A scoping review of the literature. Human resources for health, 19(1).

Freidson, E. (2017). Professional dominance: The social structure of medical care. Routledge.

Harrington, M. K. (2019a). Affordable care act. In Health Care Finance and the Mechanics of Insurance and Reimbursement (2nd ed.). Jones & Bartlett Learning (pp. 73-102).

Harrington, M. K. (2019b). Government incentive programs. In Health Care Finance and the Mechanics of Insurance and Reimbursement (2nd ed.). Jones & Bartlett Learning (pp. 223-240).

Harrington, M. K. (2019c). Managed-care organizations. In Health Care Finance and the Mechanics of Insurance and Reimbursement (2nd ed.). Jones & Bartlett Learning (pp. 103-116).

Herzig, T., & Walsh, T. (2020). Implementing information security in healthcare: Building a security program. CRC Press.

Lawrence J. Gitman, L. J., McDaniel, C., Shah, A., Reece, M., Koffel, L., Talsma, B., & Hyatt, J. C. (2018). Introduction to the business. OpenStax.

Melling, J. (2017). Preparing for value-based payment: fundamental change that encompasses the revenue cycle. Healthcare Financial Management, 71(5), 60-67.

Recovery Auditors / RACs. (n.d.). AMA. Web.

Shapiro, D., Boerner, B., Brancatelli, R., Chumney, W., Dendinger, L., Nantz, B., Poepsel, M., Byars, S. M., & Stanberry, K. (2018). Business ethics. OpenStax.

Systems of care compliance program. (2021). Department of Health and Human Resources.